|

| Key Concepts |  |

| |  | | What is the Tamar Index Universe? |

| | About 450 shares are traded on TASE; however, not all securities "fit" for inclusion in the TASE indices. Threshold criteria have been developed to define a selected population of shares eligible for inclusion in the indices. Only shares that meet these criteria are included in the indices. The list of eligible shares is called the "Tamar Index universe", or simply "Tamar".

The universe is updated semi-annually, at the close of trading day of the first Thursday in February and August. The index universe is updated according to the threshold criteria.

Following are Tamar criteria:

- Free float rate: 15%

- Minimum average free float value: NIS 40 million

- Average Price – 50 Agorot (0.5 NIS) or above

Special dispensation is granted to shares already included in the Tamar, when re-examined for maintaining their status as a universe constituent. These shares continue their constituency if they meet the following criteria:

- Free float rate: 10%

- Minimum average free float value: NIS 20 million

- Average Price – 30 Agorot (0.3 NIS) or above

Tamar index rebalance dates >

More information > | |

|

|

| | | | | | What is the Rimon Index Universe? |

| | Rimon Index universe contains shares that meet stringent criteria (approximately 220 shares), from the shares included in the Tamar universe. Only TASE flagship indices can be used as underlying assets for derivatives. The Rimon universe is updated semi-annually, at the close of trading day of the first Thursday in February and August. The index universe is updated according to the threshold criteria set.

Following are Rimon criteria:

- Free float rate: 35%

- Minimum average free float value: NIS 100 million

- Liquidity – Average daily volume 50,000 NIS Or Median daily turnover

Special dispensation is granted to shares already included in Rimon, which are re-examined for maintaining their status as a universe constituent. These shares continue their constituency if they meet the following criteria:

- Free float rate: 30%

- Minimum average free float value: NIS 50 million

- Liquidity – Average daily turnover 50,000 NIS Or Median daily turnover

For Tamar index rebalance date, click here.

For more information, click here. | |

|

|

| | | | | | Which shares are considered "New"? |

| | A share is considered new in the period that begins immediately after the seasoning period and ends on the record date of the first parameters update date that occurs after the end of the seasoning period.

The "seasoning period" lasts for 30 calendar days after a share's first trading date (IPO or Dual listing). During this period the share is not entitled to be included in the indices. | |

|

|

| | | | | | Which shares are considered "Seasoned"? |

| | A share is considered seasoned after the share transitions the first monthly parameters update record date that occurs after the end of the seasoning period. | |

|

|

| | | | | | Which shares are considered "Foreign"? |

| | A share is considered foreign if the company does not have a strong affinity to Israel. The TASE Index Committee is authorized to decide if a share that is domiciled outside the State of Israel has a strong affinity to Israel. In order to decide if a company has a clear Israeli orientation, the Index Committee takes into consideration parameters such as the scope of employment in Israel, the amount of properties owned in Israel, its Israeli dependence, etc. In cases where the Index Committee decides that the company does not have a clear Israeli orientation, the company will be considered a foreign company.

Foreign shares are only allowed to the Tamar universe and to Global indices series (For example, TA-GlobalBlueTech Index). A seasoned foreign share that is already included in the indices and universes is allowed to remain in the indices and universes until deletion, if and when applicable. | |

|

|

| | | | | | Liquidity Criterion for Inclusion in the Rimon Index Universe |

| | The liquidity criterion is one of the criteria for inclusion of shares in the Rimon index universe. The liquidity criterion is designed to ensure "sufficient" trading, which allows its inclusion in indices used as an underlying asset for derivatives. The liquidity criterion only applies if more than 150 shares meet the Rimon criteria.

The share must meet one of the following requirements:

- Average daily volume – 50,000 NIS

The determining figure is the average daily trading volume (in NIS) of the share during the six months preceding the Record Date. For example, for the update date of August 3, 2017, the average daily volume was calculated for the period that began on January 14, 2017 and ended on July 13, 2017. For a share that was traded for less than six months, the average daily volume calculation will only be for those trading days the share was listed on the Stock Exchange.

- Median daily volume – 10,000 NIS

The determining figure is the Median daily trading volume (in NIS) of the share during the six months preceding the Record Date.

| |

|

|

| | | | | | How is market capitalization calculated for the purpose of index universe eligibility? |

| | The market capitalization of a given share is one of the criteria for entry into the index universe and for constituency in market cap indices (i.e. indices for which the composition of the index is set according to the market capitalization of its constituent shares, such as the TA-35, TA-90 and other indices).

Market capitalization is calculated as follows:

MV=Q*P

MV – Market Cap of a given share on the parameter update record date. Q – Index Adjusted Number of Shares (IANS) on the parameter update record date. P – Average closing price, that equals to the average of the closing prices of a given share on ten days prior to the fixed parameter update record date. However, if the record date is not a trading day, then the average closing price of nine days is taken into account.

If the ex-dividend was calculated (following cash dividend, stock dividends, etc.) during a period of 10 trading days ending on the fixed parameter update record, the average closing price of the share is calculated so that each one of the closing prices is calculated one day prior to the ex-date, and then multiplied by the ratio between the ex-date and the record price. | |

|

|

| | | | | | IANS (Index Adjusted Number of Shares) |

| | IANS (Index Adjusted Number of Shares) – is one of the parameters used in setting the weight of a given share in the index. There are two types of IANS: Monthly IANS and Special IANS.

- Monthly IANS – Capital listed for trading of a share on the parameter update record date.

- Special IANS – IANS in cases of corporate action events such as Rights subscription, Reverse stock split, spin-off etc. TASE adjusts the IANS accordingly to reflect the change.

| |

|

|

| | | | | | Free float |

| | The free float refers to the number of shares held by the general public (i.e., not held by any party of interest). | |

|

|

| | | | | | Free Float brackets for calculating a share's weight in the index |

| | The free float rate (percentage) is the number of shares held by the public relative to listed capital for trading.

The free float rate for calculating a share's weight in the index is determined on the monthly parameter update record date. In order to increase the stability of the index, shares are segregated into 7 classes (brackets) based on their free float rate. This metric is used to calculate a share's weight in an index, as opposed to using the exact free float rate.

The following table outlines the classes and rules for entry and exit into a free float class:

Free Float Rate Range |

Index adjusted Free Float Rate (brackets) |

|---|

Under 20% |

10% |

20% |

20% – 25% |

25% |

25% – 30% |

35% |

30% – 35% |

45% |

35% – 45% |

60% |

45% – 60% |

80% |

60% – 80% |

100% |

80% – 100% |

| |

|

|

| | | | | | Free float rate for index and universe updates |

| | The free float rate is the amount of public holdings relative to the share's capital listed for trading.

The free float rate for the purpose of meeting index criteria is examined semi-annually based on the actual free float rate on the dates of June 30th and December 31st, preceding the update, as applicable.

| |

|

|

| | | | | | Free float for calculating a share's weight in the index |

| | A share's "free float" is the capital listed for trading held by the general public. The free float used for calculating the weight of a share in an index is the product of multiplying the IANS by the free float rate class. | |

|

|

| | | | | | Free float value for index and universe updates |

| | The free float value for updating indices and universes is updated semi-annually, and is the product of multiplying the following three parameters at the semi-annual update record date:

| |

|

|

| | | | | | Free float value for calculating a share's weight in the index |

| | The free float value for updating a share's weight in the Index is the product of multiplying the following four parameters:

| |

|

|

| | | | | | Weight Cap Limitation |

| | Weight caps have been placed on index constituent shares, in order to limit the impact of a single share in an index. A weight cap has been set for each index. In practice, if after the constituent shares are weighted according to the original data, the weight of one or more shares exceeds the cap set for the index, the calculation will be adjusted so as to bring the weight down to the weight cap. The mechanism which adjusts (lowers) the "original" weight of a share to the weight cap is called the weight cap factor. This factor is used to calculate the actual weight of shares in the index.

The specific weight cap limit for each index can be found in the "About Index" tab in index page. | |

|

|

| | | | | | Weight cap factor |

| | The weight cap factor is one of the parameters in the equation used in index rebalancing, which adjusts the weight of the most highly capitalized shares in an index to the weight cap set for the index.

For example, if indices did not have a weight cap imposed on them – the "original" weight of Teva Pharmaceuticals would be particularly high (as a result of the large free float value). In order to limit its weight, the original weight is adjusted by the weight cap factor.

The factor is calculated for each share in the index on a monthly basis (synchronized with monthly updates of IANS and free float for rebalancing). When the "original" weight is higher than weight cap – the factor will be less than 1.

For weight cap factor in TASE indices, click here | |

|

|

| | | | | | List of shares eligible for constructing an index |

| | The list comprises the relevant eligible shares for a given index. For example – the list for constructing the TA Real Estate Index comprises all the shares of real estate and land development companies. The list for the TA- Technology Index comprises all shares which the TASE has designated as engaged in technology, and the list for the Tel-Div index comprises all shares exceeding a certain threshold market capitalization, which have distributed at least 2% dividends in two out of the previous three years.

For a share to be included in a TASE index, it must be included in the index universe and must be on the relevant list. In cases in which the number of shares on an index is limited, such as the TA Real Estate-15, only the 15 most highly capitalized shares are selected, subject to their replacement ranking, from among those shares included on the relevant list and in the index universe. | |

|

|

| | | | | | Replacement ranking criterion |

| | For indices in which the number of constituents is limited, such as the TA-35 index, a replacement criterion has been set, according to which shares are added or deleted from the index on the semi-annual index reconstitution index update dates. The ranking is conducted on the list of shares eligible for a given index, according to the replacement criterion. Shares ranked higher than the entry threshold are included in the index, whereas shares ranked below the exit threshold are deleted from the index. In most cases, the ranking is based on average market capitalization with the exception of TA-SME60, which is ranked based on average free float capitalization.

How is a replacement conducted?

In the case of the TA-35 index, for example, shares meeting the index's threshold criteria (i.e., included in the Rimon index universe, with at least 1 billion free float value) are ranked according to average market capitalization. All shares ranked in the top 30 are included in the index. All shares ranked 40 and below are excluded from the index.

Should more than 35 shares remain, additional shares, starting with the lowest ranked, are excluded. If less than 35 shares remain, additional shares, starting with the highest ranked, are included. | |

|

|

| | | | | | What is the difference between Tracking and Benchmark Indices? |

| | A tracking index is an index designed to serve investors in portfolio management. Investors can accurately track the returns of an index by holding exactly those shares comprising the index. TASE's tracking equity indices are quoted real time throughout the trading day and include only those shares populating the index universes.

A benchmarking index is an index relating to a designated group of securities (for example, a specific industry group or sector). These indices are not normally quoted continuously and their objective is to reflect the state of the market for the given industry. TASE's equity benchmarking indices are quoted at the end of each trading day and include all TASE-traded shares grouped in different categories. | |

|

|

| | | | | | Dividend Yield |

| | The dividend yield expresses the ratio between the paid cash dividend per share and the share price (market price) at the time of distribution.

For example, a company paid dividends twice in the past year (i.e., the 12 months preceding the record index update date).

|

Dividend |

Share Price at the time of Distribution |

|---|

First Distribution |

10 Agorot (NIS 0.10) per share |

100 Agorot (1 NIS) |

Second Distribution |

12 Agorot (NIS 0.12) per share |

125 Agorot (1.25 NIS) |

In the first distribution, a dividend of 10 agarot (NIS 0.10) for each share was distributed, whereas in the second, 12 agarot per share was distributed. Share prices on the dividend distribution dates came to 100 agarot and 125 agarot respectively. In other words, the dividend yield of the share is 19.6% (10/100 + 12/125).

| |

|

|

| | | | | | Price adjustments due to a corporate actions event |

| | Following a corporate action (dividend distribution, rights, etc), the security price is lowered to adjust for the value of the net benefit to the investor. The adjusted price (ex-price) constitutes the base price of the security on the trading day following the corporate action event, which is incorporated in the calculation of the TASE indices. The logic behind this system is to adjust the value of the benefits embedded in corporate actions of the securities prices. | |

|

|

| |

| | Indices and Universes Update |

| | | | How long between the time a share is listed (IPO) and the time it is eligible for inclusion in the Universes? |

| | A share is eligible for inclusion in the universes if it is defined as new share or seasoned share.

Shares that have not yet passed the first monthly parameters update date, after 30 calendar days from the date of their listing (IPO) will not be eligible for inclusion in the universes.

Market capitalization and average daily volume of a new share will be calculated for the actual days the share has been traded on TASE.

| |

|

|

| | | | | | What types of securities are not eligible for inclusion in the Index Universes? |

| | Shares not eligible for inclusion in the Tamar index universe include:

- Delisted shares or shares for which delisting procedures have started.

- Shares for which trading has been suspended (permanent suspension).

- Shares on the Maintenance List.

- Shares that do not meet other threshold conditions of the Tamar index universe

Shares not eligible for inclusion in the Rimon index universe include:

- Shares not included in the Tamar universe

- Shares on the Illiquid list

- Non-Israeli shares (foreign shares that are already constituents will remain in the index)

- Shares that do not meet other Rimon universe criteria

| |

|

|

| | | | | | What types of securities are included in the Tamar and Rimon Universes? |

| | The index universe is comprised solely of shares and participation units.

ETNs, mutual funds, structured financial products, convertible securities (convertible bonds and warrants), etc. are not included in index universes.

| |

|

|

| | | | | | Are convertible securities counted for the purpose of calculating market capitalization or the free float? |

| | The Tamar and Rimon universes contain only equity indices. For the purpose of calculating market capitalization and the free float, only shares of the same class are taken into account. | |

|

|

| | | | | | Which indices are included in the Rimon series? |

| | Rimon series indices comprise only shares included in the Rimon universe.

Rimon series list of indices:

- TA-35 index

- TA-90 index

- TA-125 index

- TA Banks-5 index

| |

|

|

| | | | | | Which indices are included in the Tamar series? |

| | Tamar series indices comprise only shares included in the Tamar universe.

Tamar series list of indices:

- TA-AllShare Index

- TA SME-60 indexTA-Growth index

- TA-Global BlueTech index

- TA-TechElite

- TA Technology index TA Biomed index

- TA Finance index

- TA Insurance Plus index

- TA Real Estate index

- TA Oil & Gas index

- TA-Comm & information technologies index

- Tel Div index TA Maala index

- TA-35 Net USD index

| |

|

|

| | | | | | How and when is the Semi-Annual Index Composition reviewed? |

| | The reconstitution of TASE indices, i.e. the updating of the securities comprising the index, is conducted on the scheduled index reconstitution dates, or upon entry of a new share under the fast track provisions for IPOs and dual listings.

The constitution of the indices is updated at the end of the record date. This reconstitution becomes effective on the index update date. The constituency of the index universe is updated on the update date (Tamar and Rimon), along with the constituency of the indices themselves.

Only shares included in the Tamar and Rimon index universes can be included in real-time quoted equity indices.

Index Update Dates

Record Date |

Publication |

Update Date

(becomes effective) |

|---|

The Thursday three weeks prior to the update date, at end of the trading session |

The Thursday two weeks prior to update date** |

The first Thursday of August and February, at the end of the trading session. |

* The Maala index is updated annually during the August update, at the time of Tamar's August update, based on the record date data on Tamar's August update.

*The Tel-Div index is updated annually during the time of Tamar's February update, based on the record date data on Tamar's February update.

**If on that day there is no trading on the TASE or on the U.S. Stock Exchanges (NASDAQ/ NYSE), the update / publication date is on the next trading day, on which there is trading on the U.S. exchanges as well. A change in the publication date and / or update does not carry a change in the Record Date.

For the index update date, click here. | |

|

|

| | | | | | The number of securities in an index |

| | Some indices are not limited in the number of constituents, and they include all shares that meet the criteria set for the index, such as the TA-AllShare, the TA-Growth and the TA-Biomed etc. Other indices can include a restricted number of shares. The name of the index usually indicates the allowed number of shares. The TA-35, for example, is designed to include only 35 shares.

However, even for these indices, under certain circumstances, the actual number of shares may deviate from the stated number restriction between index reconstitution dates. If, for example, a share is added under the "fast track" provision (for example following an IPO or dual listing), the number of shares in the index will exceed the set restriction. Conversely, events such as mergers and tender offers can lead to a share's deletion from an index in the mid-term and the number of shares will be lower than the set restriction. Upon index reconstitution, the number of constituents as designated in the number restriction will be restored. | |

|

|

| | | | | | Free Float Value as a criterion for inclusion in an index |

| | The threshold criteria for some indices are stricter than those for inclusion in the Tamar or Rimon index universe. For example, the average free float value criterion for entry into the Tamar index universe is currently NIS 40 million. In contrast, entry into the Tel-Div index requires a minimum average free float value of NIS 400 million, while current constituents in the index must have at least a NIS 300 million average free float value to maintain their inclusion in the index. The objective of this dispensation is to ensure that this index, which is equally weighted giving a relatively higher weight to smaller shares, is comprised of sufficiently "robust" shares which are capable of "carrying the weight of the index on their shoulders". | |

|

|

| | | | | | Index components historical data |

| |

In addition, Index Components Historical Data on a daily basis can be found on the TASE website under the appropriate Index page.

- Navigate to the Index Page:

- Inside the Index Page – click on the "Index Component" Tab

- Click on other date

- Choose a date and Click OK

| |

|

|

| | | | | | What are the additional threshold conditions for inclusion in specific indices? |

| | Only those shares included in the index universe can be included in the real-time quoted equity indices. However, additional criteria apply for all indices.

For example, the TA-35 index is comprised solely of shares comprised out of the Rimon index universe with a minimum free float value of 1 Billion NIS. | |

|

|

| | | | | | Is it possible for a share to be added to an index on a day other than the index update date? |

| | Shares can be added to index universes and TASE indices under a designated fast track arrangement.

| |

|

|

| | | | | | What is the fast track for adding new shares to universes? |

| | When shares are listed on TASE for the first time, they are "fast-tracked" to an index universe. Having said that, shares included in a universe prior to the scheduled semi-annual index reconstitution date, must meet index universe criteria (excluding liquidity criterion). A share will be added to universes, if on the first monthly record date for updating parameters, which occurs 30 calendar days from the first day of listing (fast track record date), a share meets applicable index criteria. The date of addition to universes shall be the first monthly parameters update date following the fast track record date.

To simplify, here is what a typical fast track time table looks like:

- First trading day (IPO or dual listing)

- End of seasoning period (30 calendar days after the first trading day)

- First monthly parameters record date

- Monthly parameters update ("fast track entrance date")

After a share is "fast tracked" into the universes, it will be added to relevant indices under the fast track criteria to join the index, assuming additional criteria apply to specific indices.

In most cases, the criteria for adding new shares to indices through fast track are more lenient than those required when adding a seasoned share to an index. | |

|

|

| | | | | | What is the fast track for adding a seasoned share to the indices? |

| | Seasoned shares may be added to indices, once they have been added to the Tamar universe during the monthly parameters update dates, assuming they meet index criteria on the monthly parameters update record date. It is important to note that there are no fast track additions for seasoned shares during semi-annual update dates.

| |

|

|

| | | | | | What happens during a merger involving an index constituent? |

| | In mergers and acquisitions, if a company whose shares are included in an index is acquired, its shares are deleted from the index.

An announcement regarding a share's deletion from an index is published on the MAYA website (Currently Hebrew only) as well as under the index announcements area in the TASE website (English and Hebrew).

| |

|

|

| | | | | | When are unscheduled deletions from indices and universes, and what is the process governing such an unscheduled deletion? |

| | A share will be deleted from indices and universes under one of the following circumstances:

- It is delisted (as a result of a merger, tender offer, voluntary delisting, etc.)

- It is impossible to trade in it for an extended period of time (suspension of trade under certain circumstances),

- A share is transferred to maintenance list.

A share's deletion will receive prior notification on TASE's MAYA website (Currently Hebrew only) as well as under the index announcements area in the TASE website (English and Hebrew). | |

|

|

| |

| | Index Calculation and Shares Weight |

| | | | How is the index calculated? |

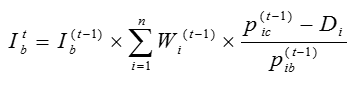

| | Most TASE indices are total return indices. Dividend yields are included in the indices and are reflected in their rate of return. No special adjustments are made by TASE to reflect the dividend yield in the total return; rather the indices' construction as total return indices is a natural outcome of the system of calculating ex-dividend share prices.

In other stock exchanges it is not customary to adjust share prices for dividend distributions, and for this reason most major indices published worldwide are price indices rather than total return indices. In most cases, total return indices, which reflect dividend yields, are calculated alongside the major indices. Indices are published with an accuracy of two decimal places.

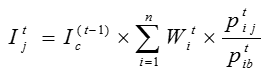

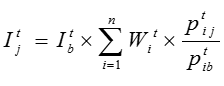

The following formula is used to calculate tracking indices:

With the exception of TA BlueChip-15Price index (Launch date TBA), that is calculated based on price method, all TASE indices are calculated on a gross total return basis.

The following formula is used to calculate price index:

Index Parameters:

It j |

Index in day t in point of time j |

I(t-1)c |

Closing index in day (t-1) |

n |

Number of shares included in the index |

Wit |

Weight of share I in the index in day t |

Ptij |

Share price of I in day t in point of time j |

Ptib |

Base price of share I in day t |

Itb |

Index base price in day t |

I(t-1)b |

Index base price in day t-1 |

Wi(t-1) |

Index's weight of share I in day t-1 |

P(t-1)ic |

Closing price of share I in day t-1 |

P(t-1)ib |

Base price of share I in day t-1 |

Di |

Ex-dividend trading day in share I – Gross dividend in Agorot paid in share i. |

| |

|

|

| | | | | | How and when are the monthly parameters updated (monthly rebalance)? |

| | The following parameters are updated for the purpose of calculating a share's weight in the index, at the end of the first Thursday of the month* ("Monthly fix parameter update record date"):

Parameter |

Mechanism |

|---|

|

Based on the listed capital for trading on the parameters record date |

|

Based on the free float rate on the parameters record date |

|

Calculated based on data on the parameters record date |

- Monthly fix parameter update record date occurs three weeks prior to the monthly fix parameter update date (monthly rebalance date).

- Monthly fix parameter publication date occurs two weeks prior to monthly fix parameter update date (monthly rebalance date)*.

*If on that day there is no trading on the TASE or on U.S. Stock Exchanges (NASDAQ/ NYSE), update date / publication date is the next trading day, which is trading on U.S. exchanges as well. Changing the publication date and / or update does not carry a change in Record Date.

For universe update dates >. | |

|

|

| | | | | | How and when is the monthly IANS (Index-Adjusted Number of Shares) updated? |

| | - Monthly IANS Update

The IANS share is updated monthly on the first Thursday of the month ("Monthly parameters update date") and it equals to the listed capital for trading on the index record update date.

- Special IANS Update

A special IANS update is designed to adjust the IANS to corporate actions affecting a share's listed equity, such as the distribution of stock dividends, rights offerings (in certain circumstances), share class unification, etc. Special IANS updates prevail over the monthly IANS updates and occur only under certain conditions.

| |

|

|

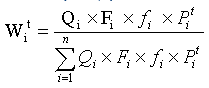

| | | | | | How are shares weighted in an index with weight caps? |

| | In indices with weight caps, shares are weighted in the index according to the following formula:

Wit |

- |

weight of share i in an index on day t |

n |

- |

number of shares in the index |

Qi |

- |

the IANS of share i on the IANS update date preceding day t, as specified below. |

fit |

- |

the weight cap factor for share i on day t |

|

|

|

Pit |

- |

base price of share i on day t |

Fi |

|

the free float rate of share i on the IANS update date preceding day t |

Fi |

- |

the free float rate of share i on the IANS update date preceding day t |

For a description of the weight cap factor and how it is calculated – click here.

For a description of the weight cap limitation – click here.

What do indices reflect?

Indices reflect average price levels of a select group of exchange-traded securities. Index fluctuations reflect the rate of return on investment for index investors, in real time throughout the trading day and over time.

On the day an index is launched a base price (in points) is set. Index fluctuations are added/subtracted from the base price in accordance with a shares' respective weights in an index. Index price level reflects all changes in an index's constituent shares.

For example, assuming that:

- The index price is 100

- The weight of a given constituent share is 5%

- A share lost 50% of its value on a certain day

- All other share prices in the index remained constant

In this case the index lost 2.5% (50% X 5%), resulting in a price level of 97.5. | |

|

|

| | | | | | Calculation frequency of Real-Time Quoted Indices |

| | Equity Indices intraday prices are calculated every 15 seconds. | |

|

|

| |

| | | | What is the VTA35? |

| | The VTA35 index measures the market's expectation of 30-day volatility implied by at-the-money TA-35 Index options prices. The index was developed according to the unique characteristics of the Tel Aviv Stock Exchange Derivatives market. VTA35 is expected to serve as the volatility barometer of the stock market. The index values represent the implied volatility in percentages (e.g., 15 points = 15%). | |

|

|

| | | | | | How is the composition of the index determined? |

| | The index is calculated as the weighted average of the implied volatility of four at-the-money options: - Call option and Put option with a time to expiration that is close to 30 days, but equal or less than 30 days;

- Call option and put option with a time to expiration that is close to 30 days, but more than 30 days.

Since, at any given time there is no at-the-money option with 30 days to expiration time, it is necessary to produce it synthetically. Therefore, the IV of the relevant options are weighted between their exercise prices and the synthetic index value and between their time to expiration and the 30-days period. In order to avoid possible deviations in the calculation results, options with minimum time to expiration of 2 days are included in index' calculation. | |

|

|

| | | | | | How is IV determined for calculating the index? |

| | The VTA35 is calculated as the weighted average of implied volatility of ATM options included in the index.

The implied volatility is calculated according to the Black & Scholes model. The following are parameters for calculating the IV according to the Black & Scholes formula: Option Price (premium) – mid price at the time of calculation (midpoint between bid and ask prices).

Underlying asset - the synthetic TA-35 index value, which is calculated as the average between the best synthetic index for buy and the best synthetic index for sale, according to the Put-Call Parity formula, according to mid prices of Call and Put options at four exercise prices around the money in the relevant series of options.

Interest rate - Bank of Israel interest rate.

Exercise price - the exercise price of the relevant option.

Time to expiration - expiration period of the relevant option. | |

|

|

| | | | | | How often is the composition of the index updated? |

| | The index is derived from ATM options that met relevant criteria at the calculation point, i.e. the set of options is updated dynamically as a function of the TA-35 synthetic index level. | |

|

|

| | | | | | How a daily close value of VTA35 Index is determined? |

| | The index' close value is calculated as the average of the VTA35 index values published during the last 5 minutes before the end of trading session in the derivatives market. | |

|

|

| | | | | | How often is the VTA35 Index calculated? |

| | VTA35 is published every 15 seconds, starting from open phase of the stock market till end of trading session in the derivatives market. | |

|

|

| | | | | | What are the possible benefits of the index? |

| | The VTA35 index can serve as an underlying asset for derivatives and / or as a benchmark for the level of volatility in the markets. | |

|

|

| | | | | | Does the volatility index tend to rise over time? |

| | Implied volatility has a tendency to mean convergence over time, unlike Equity or FI indices that behaves in a random manner, with a tendency to rise over the years, meaning that the volatility index is rising and falling over the years (for example, VIX index was in range 9-41 points in 2013-2018 years) in accordance with market volatility, but converges to the average (similar to bond yields). | |

|

|

| | | | | | Where can I see the methodology of the index? |

| |

|

| |

| | | | Historical data terminology |

| |

|

| | | | | | When did TASE begin Calculating Indices According to International Standards? |

| | TASE began float-adjusting real-time quoted indices on February 3rd, 2008. In other words, since that date, the weight of each share in TASE's real-time quoted indices is based on the value of the free float,( i.e. that portion held by the public at large, as is customary with leading indices worldwide) rather than on the market capitalization of all shares, as was the case prior to change.

TASE introduced the Index floating weight cap on July 2010. At that time, a floating weight cap was set for each quarter (the floating cap can breach the original weight cap by 50%, from a weight cap of 10% to a maximum weight cap of 15% until the quarterly rebalance). During the course of the quarter the weight of the shares that reached the weight cap reflected the rate of return since the last setting.

On February 9, 2017, TASE introduced an all new index methodology whose main goal was to reduce the concentration in the indices. As part of the all new index methodology TASE defined two equity universes (Rimon and Tamar), the indices were expanded (for example, TA-100 became the TA-125), weight caps have been significantly reduced for most of the indices, etc. For further information in regards to TASE indices, click here. | |

|

|

| | | | | | Where can I find a full description of the new TASE Index Calculation Methodology? |

| |

|

| | | | | | What is the scope of the Index Committee's discretion? |

| | The Index Committee includes TASE’s Chief Executive Officer, its Trading Manager and the Head of the Listing and Economics Department.

The Index Committee is authorized to determine the following (among others):

- Minimal free float rate for new additions to the indices and universes

- Israeli orientation for companies domiciled outside of the State of Israel

- Changes in indices and universes update dates

- Determine Index calculation frequency

- Deletion of a specific share under special circumstances

- Out of the ordinary rules under special circumstances (for example, complex corporate action events).

| |

|

|

| | | | | | What is the scope of the Index Manager's authority? |

| | TASE's Index Manager has the discretion to determine the fixed parameters for calculating a share's weight in the index. In addition, under special circumstances, the Index Manager has the discretion to change deletion or addition dates of a specific share to the index. | |

|

|

| | | | | | What do the indices reflect? |

| | Indices reflect the average price levels of a select group of exchange-traded securities. The fluctuations in share price indices reflect the rate of return on investment in them and measure the outcome of the investment for better (gains) or for worse (losses), both in real time throughout the trading day and over time.

On the day an index is launched a base price (in points) is set. Fluctuations in share prices are added/subtracted from the base price in accordance with the shares' respective weights in the index. The price level of the index reflects the sum total of changes in the index's constituent shares.

For example, assuming that:

- the index price is 100

- the weight of a given constituent share is 5%

- the share lost 50% of its value on a certain day

- all other share prices in the index remained constant In this case the index lost 2.5% (50% X 5%), resulting in a price level of 97.5.

| |

|

|

| |

|

|

|